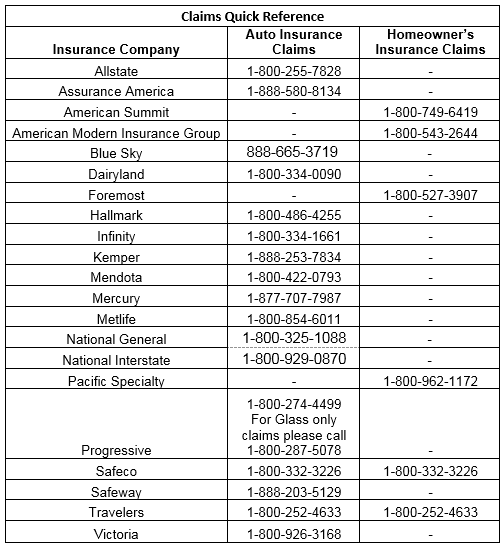

The insurance industry is weird or is it? Like any industry there are those that want to sell direct through exclusive distributors, those that wholesale through non-exclusive distributors, and those that sell direct online to the consumer. As an independent agent we work with companies that wholesale non-exclusively. Here we try to introduce you to the Insurance Companies We Represent and Why. We represent many different companies to try to ensure you get the best coverage at the best rate year after year.

The insurance industry is weird or is it? Like any industry there are those that want to sell direct through exclusive distributors, those that wholesale through non-exclusive distributors, and those that sell direct online to the consumer. As an independent agent we work with companies that wholesale non-exclusively. Here we try to introduce you to the Insurance Companies We Represent and Why. We represent many different companies to try to ensure you get the best coverage at the best rate year after year.

Thing is some people have never heard of the companies we represent. So they have to be small and unheard of, right? Not really. We actually work with some of the most reputable companies in the market. In this blog we try to give you an idea of who we represent and how large they actually are.

Let’s start with auto insurance. There is a group called the NAIC that reports how large companies are in the US. The data below is from that list.

| Auto Insurance Company Ranking by Size in 2017 | ||

| Rank | Company | Premium in Billions |

| 1 | State Farm | 41 |

| 2 | Berkshire Hathaway Grp (GEICO) | 29 |

| 3 | Progressive | 22 |

| 4 | Allstate | 21 |

| 5 | USAA | 13 |

| 6 | Liberty Mutual/Safeco | 11 |

| 7 | Farmers | 10 |

| 8 | Nationwide | 7 |

| 9 | Travelers | 4 |

| 10 | American Family | 4 |

| 11 | Auto Club (AAA) | 3 |

| 12 | Erie | 3 |

| 13 | Amtrust/National General | 3 |

| 14 | CSAA (AAA) | 3 |

| 15 | Autoowners | 2.5 |

| 16 | Mercury | 2.4 |

| 17 | Metlife | 2.4 |

| 18 | Hartford | 2.3 |

| 19 | Auto Club Michigan (AAA) | 1.7 |

| 20 | Mapfre | 1.7 |

| 21 | Kemper | 1.4 |

| 22 | Amica | 1.3 |

| 23 | Infinity | 1.2 |

| 24 | Country Ins & Financial Services | 1.1 |

| 25 | The Hanover | 1.1 |

| Bolded and italicized companies are represented by Gila Insurance Group

| ||

We represent Progressive, Allstate, Liberty Mutual, Travelers, National General, Mercury, MetLife, Kemper, and Infinity. Yes that’s right, we represent 36% of the top 25 auto insurance companies in the US. 9 of the top 25.

Let’s look at homeowners.

| Homeowners Insurance Company Ranking by Size in 2017 | ||

| Rank | Company | Premium in Billions |

| 1 | State Farm | 17 |

| 2 | Allstate | 8 |

| 3 | Liberty Mutual/Safeco | 6.4 |

| 4 | USAA | 6 |

| 5 | Farmers | 6 |

| 6 | Travelers | 3.5 |

| 7 | Nationwide | 3.2 |

| 8 | American Family | 3 |

| 9 | Chubb LTD Group | 2.7 |

| 10 | Erie | 1.6 |

| 11 | Autoowners | 1.4 |

| 12 | AIG | 1.1 |

| 13 | Metlife | 1.1 |

| 14 | Progressive | 1 |

| 15 | Hartford | 1 |

| Bolded and italicized companies are represented by Gila Insurance Group | ||

With homeowner’s insurance there are still a lot of companies, but they tend to get small quick. We are going to focus on only those that write over 1 billion dollars in insurance, which leaves us with the top 15 carriers. We represent Allstate, Safeco, Travelers, and MetLife. Of the top 15 homeowner’s carriers Gila Insurance Group represents 27% of the top 15.

With 36% of the top auto carriers and 27% of the homeowner’s carriers represented by Gila, the question stands… why would you need to go anywhere else?

Remember we shop these carriers to ensure you get excellent coverage at an affordable price. If one of these companies decides to drastically change your rate, we will monitor that and start shopping the rate for you. Each of the companies we represent and work with are large recognized carriers with the financial stability to be there when you have a claim.

We can provide quotes for many of these companies online at GilaInsurance.com.

Somewhere along the way people started asking for “full coverage.” Usually this coverage refers to what an

Somewhere along the way people started asking for “full coverage.” Usually this coverage refers to what an

Some coverage is hard to explain, it’s much easier to just say see! That is exactly the case with debris removal. Debris removal isn’t difficult to explain, it’s just the cost to remove the pile of trash your insurance claim just left. If there is a fire, it’s going to be the ashes and rubble, but also the mess the fire department caused while putting it out. Let’s be real they are great a putting out fires, but they aren’t exactly tidy. If there is a flood, we might be looking at all the damaged drywall and installation. Some of it might be moldy or muddy. The point is there is a cost to haul it away. But there is also going to be a cost for the demolition, which can get pretty costly.

Some coverage is hard to explain, it’s much easier to just say see! That is exactly the case with debris removal. Debris removal isn’t difficult to explain, it’s just the cost to remove the pile of trash your insurance claim just left. If there is a fire, it’s going to be the ashes and rubble, but also the mess the fire department caused while putting it out. Let’s be real they are great a putting out fires, but they aren’t exactly tidy. If there is a flood, we might be looking at all the damaged drywall and installation. Some of it might be moldy or muddy. The point is there is a cost to haul it away. But there is also going to be a cost for the demolition, which can get pretty costly. Debris removal is usually included in most property insurance policies, but like most things with an insurance policy there are limits. Depending on where it is commercial insurance or a homeowner’s policy it can vary, but here are some things to consider when it comes to debris removal. How unique is your building? How old is your building? How much space is around your building. All of these and more can cause additional costs in removing debris from your property. Another consideration is building materials. Is there any asbestos in the building? The cost of asbestos disposal adds additional cost to debris removal.

Debris removal is usually included in most property insurance policies, but like most things with an insurance policy there are limits. Depending on where it is commercial insurance or a homeowner’s policy it can vary, but here are some things to consider when it comes to debris removal. How unique is your building? How old is your building? How much space is around your building. All of these and more can cause additional costs in removing debris from your property. Another consideration is building materials. Is there any asbestos in the building? The cost of asbestos disposal adds additional cost to debris removal. Insurance companies can rightly be described as technological dinosaurs. I mean for years one company has been extolling the virtues of getting a quote in 15 minutes. On a side note did you know you can get a quote from multiple companies on GilaInsurance.com in just a few minutes as well? Again, dinosaurs. I mean my patience for 30 second in a microwave is almost nil. Don’t even get me started on when the internet decides to have a traffic jam (super highway. It’s supposed to be a super highway, that means no buffering, right?). Moreover, in our office we have often made the joke that we are in the tree killing business. Why because it seems that insurance companies feel the need to print reams and reams of paper of stuff that you will likely never read (Gila Insurance Group LLC does not endorse this practice and highly encourages you to read your policy the writer was unwittingly feeling that pragmatism was witty). My favorite is the part of the insurance policy that states this page is left intentionally blank… why?

Insurance companies can rightly be described as technological dinosaurs. I mean for years one company has been extolling the virtues of getting a quote in 15 minutes. On a side note did you know you can get a quote from multiple companies on GilaInsurance.com in just a few minutes as well? Again, dinosaurs. I mean my patience for 30 second in a microwave is almost nil. Don’t even get me started on when the internet decides to have a traffic jam (super highway. It’s supposed to be a super highway, that means no buffering, right?). Moreover, in our office we have often made the joke that we are in the tree killing business. Why because it seems that insurance companies feel the need to print reams and reams of paper of stuff that you will likely never read (Gila Insurance Group LLC does not endorse this practice and highly encourages you to read your policy the writer was unwittingly feeling that pragmatism was witty). My favorite is the part of the insurance policy that states this page is left intentionally blank… why? Do you require your tenants to carry renters insurance? If not, you should. Why? Because it matters. I have a cousin that is a defense lawyer for a large insurance company. He defends them for liability cases. He has seen ALL sorts of crazy situations, and has a way of telling the story. The other day, he was explaining a situation that caught my attention. Landlords rents to a family. Tenants have a dog that would “never bite anyone.” Dog bites a kid. Takes a chunk out of his calf. The landlord was smart, and required his tenants to carry renters insurance. The limits the renters had weren’t high, but the hospital bill was covered. Good for the landlord, right? Wrong. Landlord also gets sued. Why, because while the hospital bills were covered there was some pain and suffering that wasn’t. So, naturally it would be the landlord’s responsibility for having allowed such a vicious dog to be on the premise. The verdict in this case was still pending when I spoke with him. But the outcome is irrelevant. He was their defending the insured, which brings up 3 things we can learn.

Do you require your tenants to carry renters insurance? If not, you should. Why? Because it matters. I have a cousin that is a defense lawyer for a large insurance company. He defends them for liability cases. He has seen ALL sorts of crazy situations, and has a way of telling the story. The other day, he was explaining a situation that caught my attention. Landlords rents to a family. Tenants have a dog that would “never bite anyone.” Dog bites a kid. Takes a chunk out of his calf. The landlord was smart, and required his tenants to carry renters insurance. The limits the renters had weren’t high, but the hospital bill was covered. Good for the landlord, right? Wrong. Landlord also gets sued. Why, because while the hospital bills were covered there was some pain and suffering that wasn’t. So, naturally it would be the landlord’s responsibility for having allowed such a vicious dog to be on the premise. The verdict in this case was still pending when I spoke with him. But the outcome is irrelevant. He was their defending the insured, which brings up 3 things we can learn. Understanding what’s not covered on your insurance policy lets you know what other insurance coverage you might need. Here are some of the BIG Exclusions.

Understanding what’s not covered on your insurance policy lets you know what other insurance coverage you might need. Here are some of the BIG Exclusions. Homeowner’s Insurance Coverage A is the part of the policy that covers the home or dwelling itself. That seems simple enough, but wait, there’s more. It also covers any structure that is physically attached to the building. By that it means that it can’t be connected by a fence or a utility line, but rather physically attached to the dwelling. This may include attached decks, carports, patio covers.

Homeowner’s Insurance Coverage A is the part of the policy that covers the home or dwelling itself. That seems simple enough, but wait, there’s more. It also covers any structure that is physically attached to the building. By that it means that it can’t be connected by a fence or a utility line, but rather physically attached to the dwelling. This may include attached decks, carports, patio covers.